All monetary figures in U.S. greenback fixed foreign money.

Highlights

U.S. ADR grew on the charge of inflation for a second consecutive week

First optimistic U.S. RevPAR comp for the reason that finish of August

Development centered in High 25 Markets from Wednesday onwards

Faculty soccer lifted many smaller markets

Weekend lifted by straightforward comp (Yom Kippur) and begin of fall break

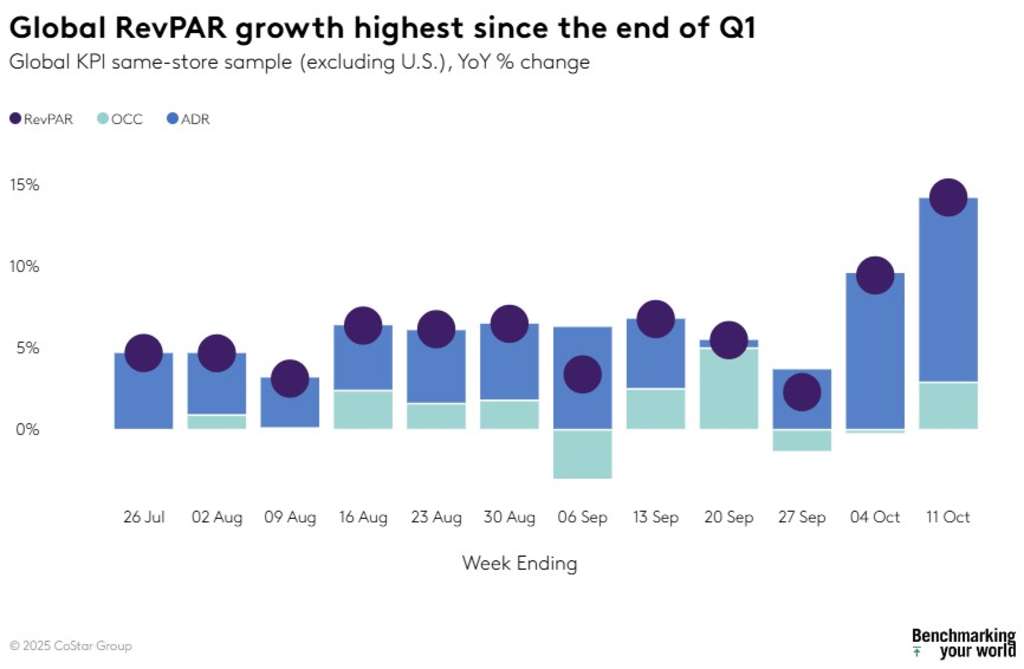

Highest world RevPAR acquire for the reason that finish of Q1

ADR surges from Tuesday onwards

For the second consecutive week, common each day charge (ADR) rose on the charge of inflation, up 2.6% for the interval ending 11 October 2025. Because of this, U.S. income per obtainable room (RevPAR) rose 0.6%, marking the business’s first weekly improve for the reason that finish of August. Occupancy, nonetheless, fell for a sixteenth straight week, with the newest decline (-1.4 share factors) half of what had been seen within the earlier fortnight (~2.5ppts).

The ADR acquire was a shock given the typical improve of +0.2% within the earlier 21 weeks (ending 27 September). Additionally, not like the earlier week when the measure rose 2.7% as a result of a big convention in Las Vegas, the end result was widespread. The High 25 Markets elevated 2.8%, regardless of a loss in Las Vegas, and the rest of the nation was up 2.4%.

Just like the earlier week, we may categorize the ADR acquire as an outlier. The measure rose a mere 0.8% from Sunday to Tuesday. On Wednesday and Thursday, ADR was up 2.8% on a 4.1% improve within the High 25 Markets. The weekend (Friday & Saturday) noticed ADR surge to 4.0% as a result of a 4.1% acquire in non-High 25 Markets, whereas the High 25 noticed a 3.8% development.

Weekend RevPAR up on robust ADR development

Thirty-one markets noticed double-digit beneficial properties over the weekend, probably the most for the reason that finish of March, led by Madison with an 81% weekend ADR acquire because of the Wisconsin-Iowa soccer matchup. Like with Madison, many of the 31 markets had been exterior the High 25 and most hosted a university soccer recreation.

The weekend was additionally lifted by a considerably straightforward comp to final 12 months’s Yom Kippur observance, which started on Friday and ended Saturday a 12 months in the past. One other contributing truth was the beginning of the Columbus Day vacation weekend. The vacation didn’t shift from final 12 months, however primarily based on STR’s College Break Report, this previous weekend was the beginning of the Fall Break for 16% of all Ok-12 college students, which would be the largest share of scholars on vacation this fall.

A 12 months in the past, this matching Saturday was the top of the Fall Break peak. General, weekend RevPAR elevated 5.0% with the High 25 Markets (+5.8%) outperforming the remainder of the nation by 130 foundation factors.

Group demand beneficial properties drive High 25 Markets

The High 25 ADR surge on Wednesday and Thursday (+4.2%) was vital, however RevPAR over these two days elevated simply 1.7% with a drag from Las Vegas. Excluding Las Vegas, RevPAR on these two days was up 5.5% on a 6.8% ADR acquire.

Atlanta, Boston, New York, San Francisco, and Tampa all noticed double-digit development in ADR with Orlando (+8.0%) and Chicago (+7.7%) additionally seeing stable development. Tampa posted the biggest RevPAR development on these two days as a result of straightforward comps from final 12 months’s Hurricane Milton, which got here ashore south of the town on Wednesday, 9 October and powerful group demand. San Francisco additionally had an amazing week with RevPAR up 24.0% on these two days and about the identical for the whole week (+24.7%) on practically a 50% improve in Group demand.

Group demand for the High 25 Markets on Wednesday and Thursday was up 13.7% excluding Las Vegas, which was down. Amongst Higher Upscale class motels, Group demand on Wednesday and Thursday grew 12% among the many High 25 Markets, excluding Las Vegas.

Placing all of it collectively, RevPAR from Wednesday onwards was up 7.5% within the High 25 Markets (excluding Las Vegas) on 6.6% ADR development. With Las Vegas, the High 25 was up 3.9% on a 4.0% ADR push.

RevPAR initially of the week for the foremost market group was down 3.2% on falling occupancy and flat ADR, and fewer so with out Las Vegas. For the whole week, High 25 RevPAR grew 1.1%. Exterior of the High 25 Markets, weekly RevPAR was flat (+0.3%) as a result of weak point initially of the week. From Wednesday to Saturday, the measure elevated 1.8% within the non-High 25.

With robust Group demand throughout the High 25, it’s not shocking that Luxurious and Higher Upscale class motels noticed the biggest RevPAR acquire within the week (+6.3% and +3.8%, respectively) with the beneficial properties considerably increased on Wednesday via Saturday, particularly within the High 25 Markets. All different resort sorts noticed RevPAR fall within the week with Financial system dropping 9.1%.

International RevPAR rushes ahead

International RevPAR on a same-store foundation confirmed its largest development for the reason that finish of the primary quarter, rising 14.2% on ADR (+11.3%). All the important thing nations and remaining areas reported RevPAR beneficial properties led by France (+43.9%) by way of Spring/Summer season Style Week finale in Paris.

India, Japan, Germany, the Center East Africa area, Spain and Canada all noticed double-digit RevPAR will increase.

Whereas France’s robust same-store RevPAR development was centered in Paris (+54.4%), all however one of many remaining markets noticed RevPAR development starting from +5.3% in Hauts-de-France to +34.8% in Provence-Alpes-CDA. The one market in arrears was Bretagne (-4.0%), which noticed decreased occupancy offset a 5.0% ADR improve. Not shocking, France’s luxurious motels noticed the biggest weekly RevPAR improve (+66.0%) with Paris Luxurious motels rising 73.0%.

All Japanese markets had been up this week with Tokyo RevPAR advancing 23.8%. Nonetheless, Osaka continued to steer the nation with same-store RevPAR up 58.3% on a 41.0% improve in ADR. As seen since April, Expo 2025 drove the beneficial properties, however they need to gradual as Expo concluded on 13 October.

Canadian same-store RevPAR superior by its largest quantity of the previous 10 weeks (+10.9%) with half of the expansion coming from ADR. Toronto and Vancouver noticed RevPAR development of 15% or extra with Quebec rising 20.0%. All three noticed stable will increase in each occupancy and ADR. Of the bigger cities, Montreal’s RevPAR was on the weaker aspect, however nonetheless up (+3.6%) as a result of flat ADR. On a complete business foundation, Canadian RevPAR grew 12.8%, totally on ADR. Like within the U.S., luxurious properties led the business in development (+23.4%), however not like the U.S., RevPAR in all resort sorts rose.

Will we see ADR drive RevPAR subsequent week?

The final two weeks have been a pleasant ADR respite, however is it sustainable? With occupancy nonetheless on the decline regardless of will increase in different journey indicators, it appears unlikely that ADR will proceed to develop at or above the speed of inflation. Nonetheless, given a positive calendar and the power in Group demand, particularly within the High 25 Markets, ADR would possibly exceed expectations for the month.

About CoStar Group, Inc.

CoStar Group (NASDAQ: CSGP) is a number one supplier of on-line actual property marketplaces, info, and analytics within the property markets. Based in 1987, CoStar Group conducts expansive, ongoing analysis to supply and keep the biggest and most complete database of actual property info. CoStar is the worldwide chief in industrial actual property info, analytics, and information, enabling purchasers to investigate, interpret and acquire unmatched perception on property values, market situations and availabilities. Residences.com is the main on-line market for renters looking for nice condominium houses, offering property managers and house owners a confirmed platform for advertising their properties. LoopNet is probably the most closely trafficked on-line industrial actual property market with 13 million common month-to-month world distinctive guests. STR supplies premium information benchmarking, analytics, and market insights for the worldwide hospitality business. Ten-X gives a number one platform for conducting industrial actual property on-line auctions and negotiated bids. Properties.com is the quickest rising on-line residential market that connects brokers, patrons, and sellers. OnTheMarket is a number one residential property portal in the UK. BureauxLocaux is among the largest specialised property portals for getting and leasing industrial actual property in France. Enterprise Immo is France’s main industrial actual property information service. Thomas Day by day is Germany’s largest on-line information pool in the true property business. Belbex is the premier supply of economic area obtainable to let and on the market in Spain. CoStar Group’s web sites attracted over 163 million common month-to-month distinctive guests within the third quarter of 2024. Headquartered in Washington, DC, CoStar Group maintains workplaces all through the U.S., Europe, Canada, and Asia. Every now and then, we plan to make the most of our company web site, CoStarGroup.com, as a channel of distribution for materials firm info. For extra info, go to CoStarGroup.com.

This information launch consists of “forward-looking statements” together with, with out limitation, statements relating to CoStar’s expectations or beliefs relating to the long run. These statements are primarily based upon present beliefs and are topic to many dangers and uncertainties that would trigger precise outcomes to vary materially from these statements. The next elements, amongst others, may trigger or contribute to such variations: the chance that future media occasions won’t maintain a rise in future occupancy charges. Extra details about potential elements that would trigger outcomes to vary materially from these anticipated within the forward-looking statements embrace, however usually are not restricted to, these acknowledged in CoStar’s filings sometimes with the Securities and Alternate Fee, together with in CoStar’s Annual Report on Type 10-Ok for the 12 months ended December 31, 2023 and Varieties 10-Q for the quarterly durations ended March 31, 2024, June 30, 2024, and September 30, 2023, every of which is filed with the SEC, together with within the “Threat Components” part of these filings, in addition to CoStar’s different filings with the SEC obtainable on the SEC’s web site (www.sec.gov). All forward-looking statements are primarily based on info obtainable to CoStar on the date hereof, and CoStar assumes no obligation to replace or revise any forward-looking statements, whether or not because of new info, future occasions or in any other case.

View supply

{kind=link}